Did you know all three national credit bureaus offer some kind of identity theft protection service? This is handy if you need something to watch over your financial records and alert you when anything fraudulent arises. There are plenty of great identity theft services that include three-bureau credit monitoring as a feature. However, with services like IdentityForce, you’re cutting out the middleman and getting the details directly from the source.

We know what you’re thinking – this type of service must be expensive. The good news is that it’s actually quite affordable. Plus IdentityForce comes with extra features like 24/7 dark web monitoring, a VPN for your mobile, and malware protection for PCs. IdentityForce will even assign you a dedicated restoration service to help manage the damages if someone steals your data. Let’s go through each of their plans in detail and see which one is going to give you the best bang for your buck.

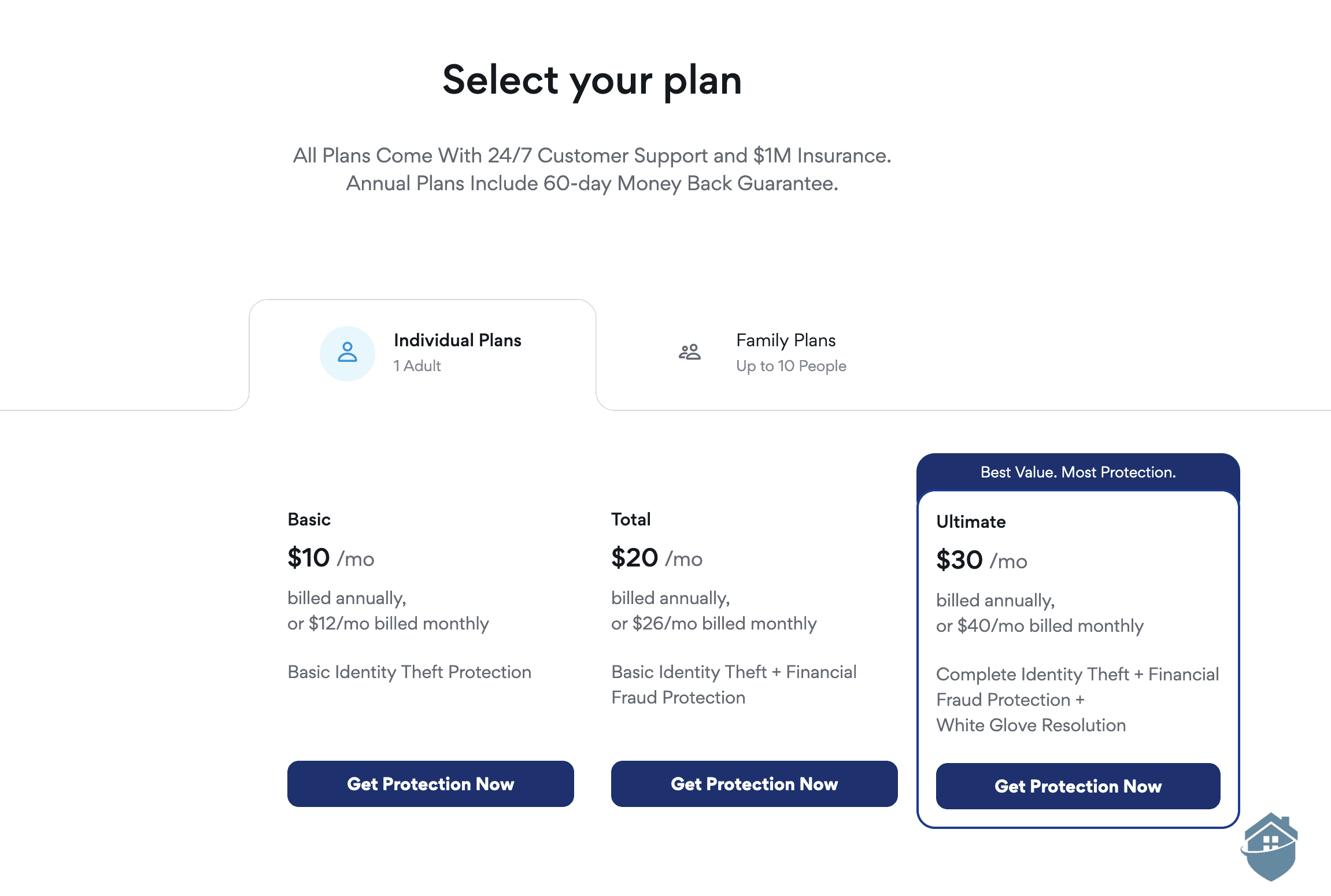

Thankfully, we found the IdentityForce pricing options to be fairly easy to follow. There are two main plans to choose from: the entry-level plan is called UltraSecure, and the higher-end option is called UltraSecure + Credit. Both are available for individuals as well as for families, which can include up to two adults and unlimited children. As you might expect, the major difference between the two plans is the credit monitoring feature. We’ll lay out the details after we look at the prices.

IdentityForce Plan

Monthly price

Annual price

UltraSecure

$19.90 per month

$199.90 per year

UltraSecure Family

$24.90 per month

$249.90 per year

UltraSecure + Credit

$34.90 per month

$349.90 per year

UltraSecure + Credit Family

$39.90 per month

$399.90 per year

Pro Tip: Protect yourself. Americans lost over $47 billion to identity fraud in2024.1 Research also shows that the older you are, the more money you’re likely to lose per incident. For example, victims in their 70s lost roughly $1,000 per incident whereas those in their 20s lost $417 per incident.

There are two pricing options for each main plan. That is, you can pay either by the month or by the year. Sure, you’ll save some of your hard-earned money by going with the annual plan, but it’s also less flexible than paying month-to-month.

Our recommendation? Start with a monthly plan to try the service out. If you like it and want to stick around, switch to a yearly plan. You’ll save money over the year with either the UltraSecure or UltraSecure + Credit plan. There is also a 30-day free trial to test things out before handing over your credit card.

Speaking of the family plans, they make the most sense if you’re part of a large family, but not so much for smaller families (for example, if you’re a single parent with just one or two children). In this instance, you might be better off looking at Aura’s plans. A Kids plan is just $10 per month and covers unlimited children across unlimited devices. You can combine it with an Individual policy, which is just $12. Plus, you’ll even get a lot of extra features with Aura that are only available in the more expensive IdentityForce plan.

Lock In an Annual Rate Risk-Free

With LifeLock, you can start with an annual plan while avoiding an immediate commitment since it comes with a 60-day money-back guarantee and 30-day free trial.

SecureScore™:

9.7/10This rating is derived from our editorial team's research, hands-on product testing, and customer surveys.

After getting hands-on experience with the service, we gave IdentifyForce strong marks in almost every category. With that said, you’ll want to pay close attention to the features offered in each plan.

Again, you’ll choose between the UltraSecure and UltraSecure + Credit plans. These options are actually quite similar, the only major difference being that UltraSecure + Credit includes credit monitoring features (three-bureau credit monitoring and access to credit reports). As you’ll see, we strongly recommend having credit monitoring in place — especially across all three credit bureaus.

IdentityForce – Monitored Accounts

UltraSecure

UltraSecure is a solid identity monitoring option that skips most credit-related features. We found it to be slightly cheaper than most options that include credit monitoring, but it still includes lots of non-credit identity monitoring features.

Fortunately, UltraSecure comes with Social Security Number monitoring. It also includes a light version of credit monitoring, which would alert you if someone requested your credit report. We think you’ll appreciate this — as it’s important to know right away if a criminal is attempting to take out a loan or apply for a credit card in your name. IdentityForce also keeps an eye on public records, the web, and the dark web to see if your sensitive information is being used fraudulently.

Combined, we think these features make UltraSecure a stronger entry-level plan than alternative options offered by top brands like Zander Insurance or Identity Guard. Zander and Identity Guard focus more on identity theft recovery and insurance, and less on credit monitoring.

FYI: It takes a special browser just to access sites on the “dark web.”2 These sites are very secure and anonymous, but that can be a bad thing when they’re used by criminals who want to avoid the prying eyes of the law.

Some of our other favorite features of the IdentityForce UltraSecure plan include the mobile app and “online PC protection tool” to help cover our digital security needs.

IdentityForce – Email Monitoring Alert

UltraSecure also includes certain features we don’t typically see in entry-level plans. These include sex offender registry monitoring and social media monitoring features.

IdentityForce – Resources Page

We even had the option for IdentityForce to monitor our bank accounts and credit cards — not bad for a basic plan. All in all, if you’re looking for foundational coverage, UltraSecure is a solid starting point. That said, if you do fall victim to identity theft, you may need the expanded insurance coverage offered in the UltraSecure + Credit plan.

UltraSecure + Credit

You can probably tell from the name of this bundle that it includes credit features (we appreciate when companies are direct). We really enjoyed trying out this service. The UltraSecure plan will notify you if (or when!) your credit is pulled for a credit check, but UltraSecure + Credit will let you check your credit report yourself. This plan also comes with three-bureau credit monitoring, as well as access to credit scores.

Did You Know? The scores we get from UltraSecure + Credit use the VantageScore metric. VantageScore is similar to FICO, as it takes all three bureaus into account to calculate a score.

Credit monitoring is an important feature. While identity monitoring tells you if your information may have been compromised, credit monitoring tells you if that information is used in actions that could damage your financial security and credit reputation. For example, IdentityForce will alert you if a bad actor applies for a credit card or takes out a loan in your name. With that knowledge, you’ll be able to lock down your credit to prevent any further financial damage.

We like that IdentityForce lets you access credit scores and reports, too. Not just because it catches thieves in the act, but also so we could see if we would run into issues taking out loans. It’s the same information the banks use to assess loans and mortgages, so we could see if there was a chance of it getting denied before showing up to our appointment.

Did You Know? Crooks can use children’s social security numbers to apply for credit cards, loans, and even government benefits. Fraud like this can go undiscovered for years and be a major chore to clean up later. The good news is that child identity theft is very rare.3 Nevertheless, we recommend that you cover your kids just in case.

The Value of IdentityForce

If money is not an issue, we think IdentityForce should be one of the identity theft protection services you should consider. But what if money is an issue? Well, that’s a different story.

But what if money is an issue? Well, we think that’s a little We even had the option for IdentityForce to monitor our bank accounts and credit cards — not bad for a basic plan. All in all, if you’re looking for foundational coverage, UltraSecure is a solid starting point. That said, if you do fall victim to identity theft, you may need the expanded insurance coverage offered in the UltraSecure + Credit plan. also like to see spouse monitoring, but we guess you can’t have it all!

At $34.90 per month, we think that the UltraSecure + Credit plan offers solid value. It’s not a bargain-basement option like Zander, but it’s fairly priced for what you get. In our experience, IdentityForce’s top-tier coverage is the much better deal of the two plans.

Yes, IdentityForce offers family protection plans. These plans protect two adults and unlimited children with a starting price of $24.90 per month. That makes it a solid pick for protecting your whole household with one subscription.

The basic plan is $19.90 per month, while the advanced plan is $34.90 per month. We recommend going premium, as the basic plan doesn’t include credit monitoring.

With a decade of experience as a journalist, Derek Prall has been covering home security for over three years. He has spent more than 1,000 hours researching security solutions and has covered almost 100 topics related to home safety. Previously, Derek has covered tech issues at American City & County magazine, where he won numerous national awards for his coverage. Derek graduated with dual bachelor’s degrees in English and Communications from Furman University and now lives in Atlanta, Georgia, with his wife and two cats.