SafeHome.org may receive compensation from some providers listed on this page. Learn More

We may receive compensation from some providers listed on this page. Learn More

SafeHome.org may receive compensation from some providers listed on this page. Learn More

We may receive compensation from some providers listed on this page. Learn More

After testing the best credit monitoring services based on ease of use and critical features, we learned LifeLock is the best choice.

Updated July 13, 2026

copied!

Updated July 13, 2026

copied!

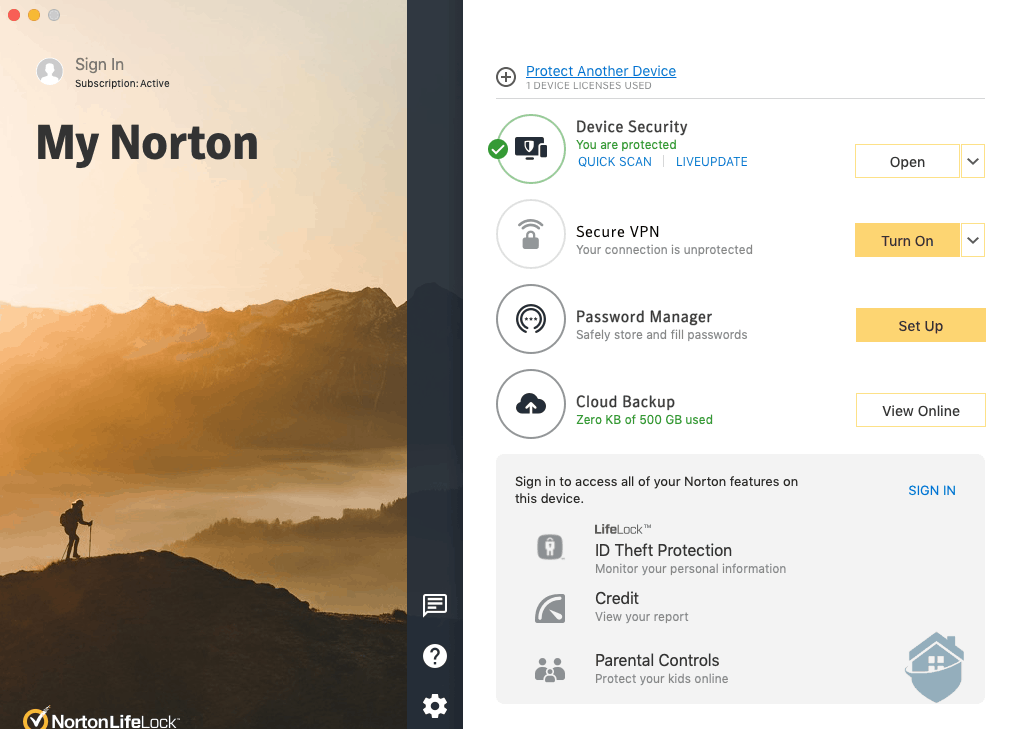

Brought to you by one of the biggest names in cybersecurity protections, LifeLock keeps your credit and finances secure by prioritizing your digital privacy to ensure fraudsters never get their hands on your personal information in the first place.

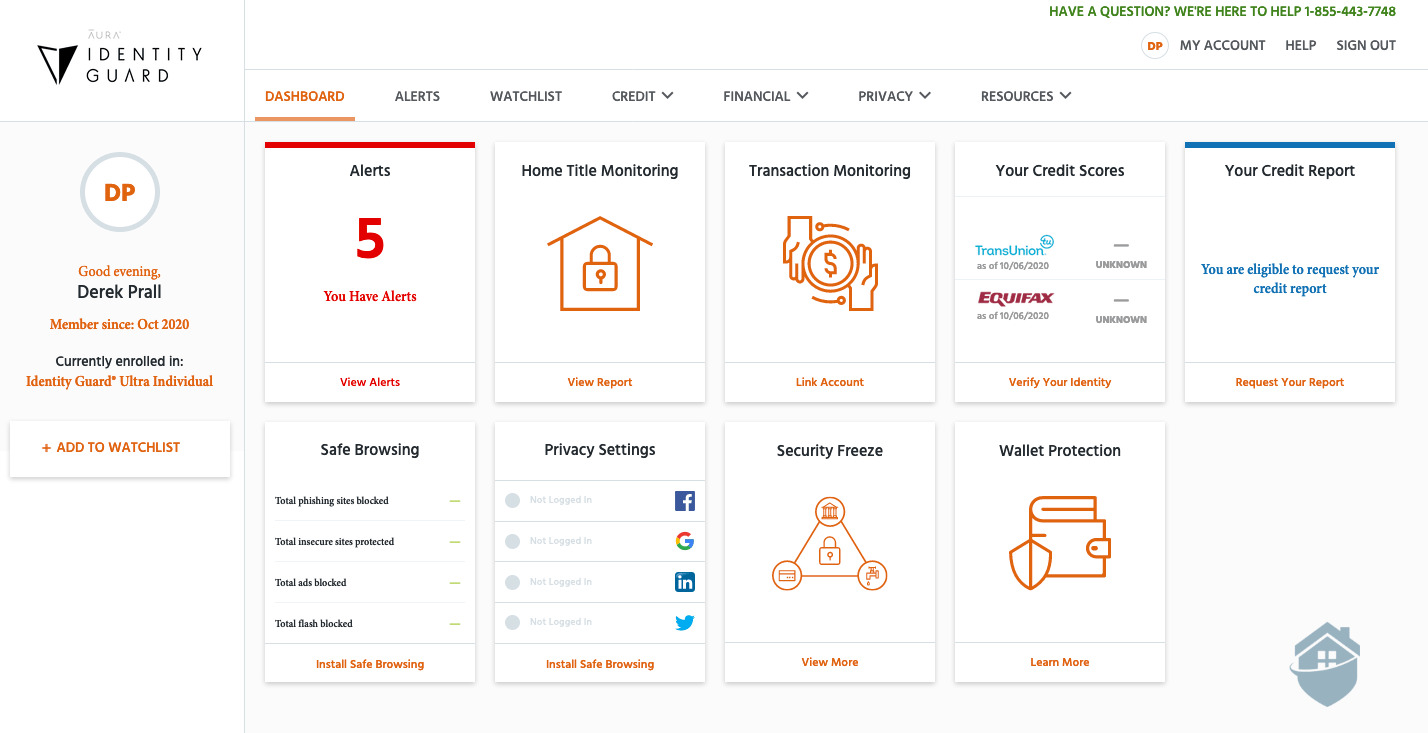

Aura offers a three-in-one VPN, password manager, and identity protection service with some of the best credit monitoring we’ve seen. Add to that financial monitoring and a user-friendly dashboard, and you’ve got yourself an effective identity theft product.

IdentityGuard is one of our top-rated services for monitoring and protecting your credit. They utilize state-of-the-art artificial intelligence powered by IBM’s Watson platform to proactively look for and respond to threats.

Picture saving up for your first home, only to find your credit score has cratered without warning. You thought you were sitting in the mid-700s, but it's actually down in the low 400s, and suddenly your mortgage plans are on hold. Scenarios like this happen more often than people realize, usually because credit isn't being monitored closely enough to catch the problem early. Fraudsters count on exactly that gap, and the fallout can be serious.

That's where identity theft protection services come in. Real-time alerts, credit monitoring, and recovery assistance work together to keep tabs on your financial health and give you a chance to act before things spiral. After thousands of hours testing and reviewing the market, we've narrowed it down to six best identity theft protection services that excel at safeguarding your credit and keeping you informed.

LifeLock earns its place as one of our favorite services on the market on cybersecurity protections alone. It pairs robust financial account scanning, three-bureau credit monitoring, and personally identifying information (PII) alerts with a comprehensive suite of digital privacy tools, adding up to one of the most well-rounded protection packages available anywhere.

When we reviewed LifeLock, we were blown away by their prioritization of your cybersecurity. They offer everything from traditional antivirus software to encrypted password vaults to virtual private network access. With these protections in place, LifeLock is all but guaranteeing that your data won’t get into the wrong hands.

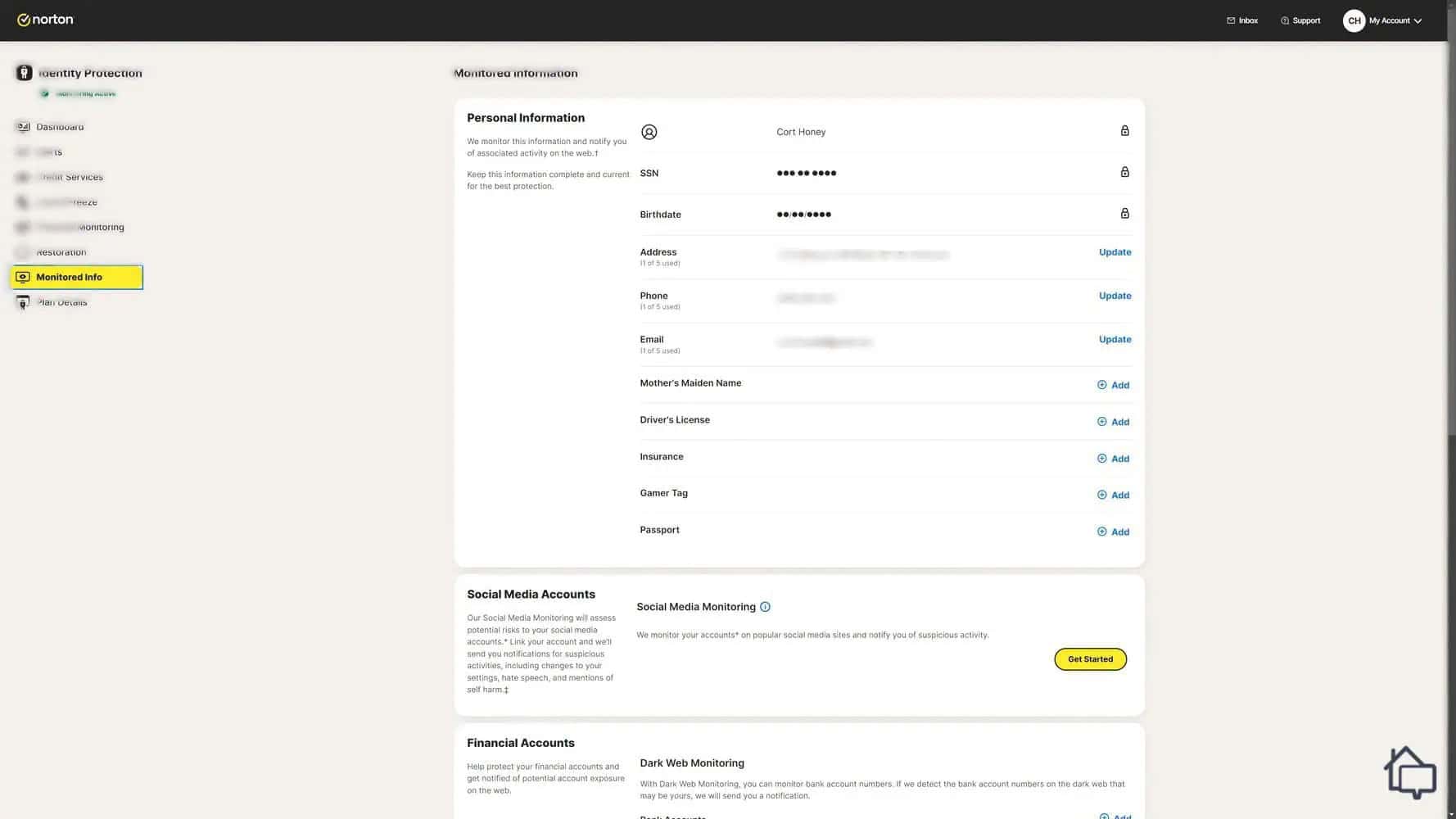

If your data somehow ends up in the wrong hands anyway, LifeLock still has you covered. It monitors all three credit bureaus on its premium tiers, giving you full access to your credit reports and scores so you can spot discrepancies fast. LifeLock also continuously scans your financial accounts and balances for unusual activity. If someone does get in, you’ll hear about it right away. Even if a fraudster still manages to pull one over on you despite all those layers of protection, LifeLock’s reimbursement coverage has your back, with up to $3 million in coverage depending on your plan.

LifeLock’s standout feature is its fictitious identity monitoring, which targets synthetic identity theft, a fast-growing fraud tactic where criminals blend real and fabricated personal details to create an entirely new identity. It’s a type of fraud most competitors don’t actively monitor for, which makes this one of LifeLock’s more genuinely differentiated protections.

They offer a broad array of services packages and pricing plans, so be sure to check out our guide to LifeLock costs and packages to find the plan that’s right for you.

Did You Know? It’s important to keep a close watch on your credit reports, even if it seems like a chore. Consumers submitted approximately 1.1 million identity theft reports in 2024 to the FTC, and even more people have errors on their credit reports.1

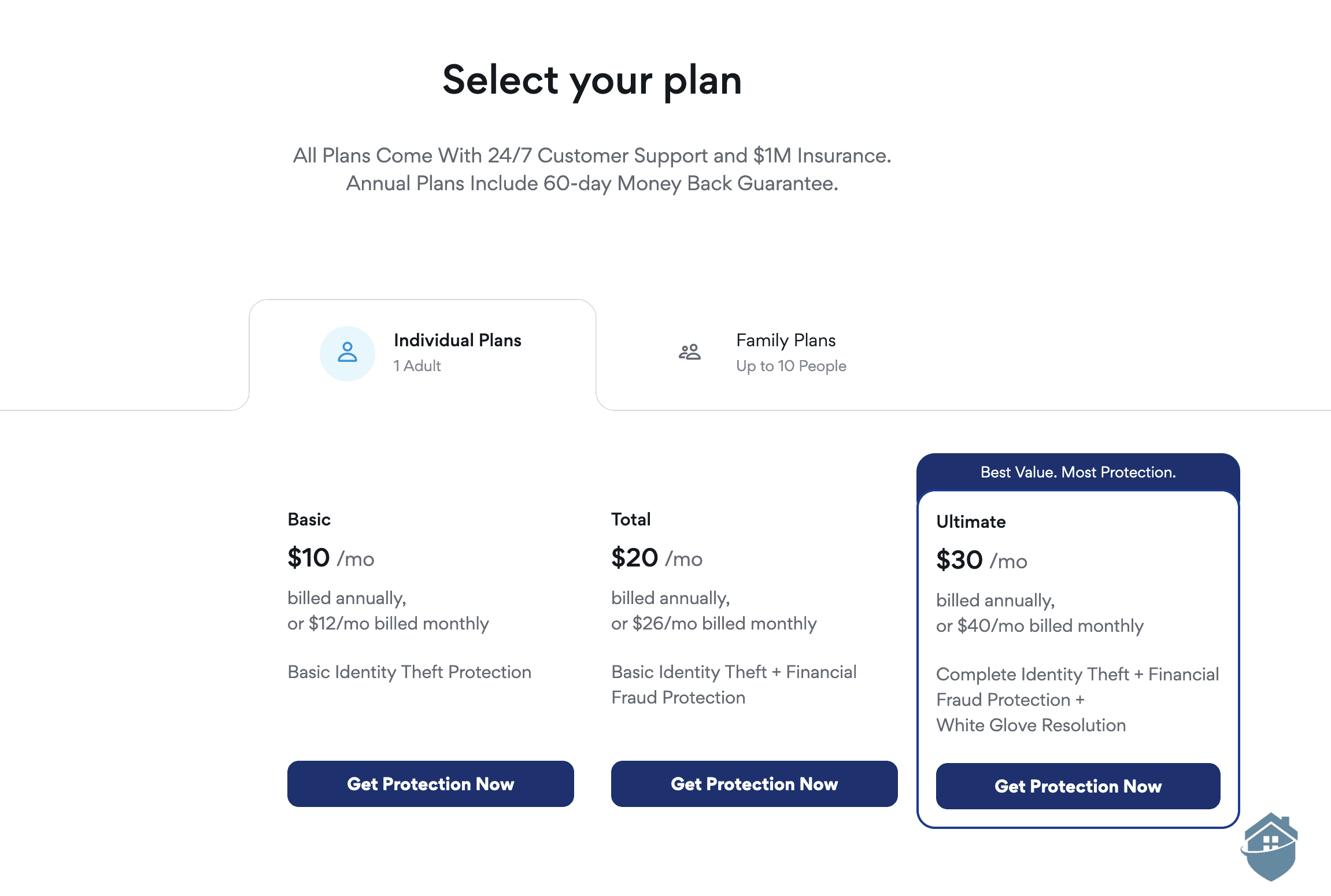

| Identity monitoring | Yes |

|---|---|

| Credit monitoring | 2-bureau (Core), 3-bureau (Advanced, Total) |

| Insurance | Up to $1.05M (Core), $1.2M (Advanced), $3M (Total) |

| Free trial | 30 days |

| Money-back guarantee | 60 days (annual plans), 14 days (monthly plans) |

Aura earns a spot on our list of best credit monitoring services with its comprehensive credit monitoring and feature set. It spans from device-level protection to financial account monitoring. The platform monitors credit reports from all three major credit bureaus, Experian, Equifax, and TransUnion, offering broader coverage than single-bureau monitoring services and giving you a fuller picture of your financial health.

When we reviewed Aura, what impressed us most was just how much ground it covers in protecting identity and finances. It’s one of the most comprehensive feature sets we’ve seen, and we’ve seen plenty of identity protection services by now.

Aura starts with malware protection, shielding you from credit and identity fraud through the antivirus software bundled into the service. A virtual private network is included too, which helps prevent hackers from intercepting financial data over unsecured public Wi-Fi.

Financial account coverage is similarly thorough. Aura monitors nearly everything, from bank, 401(k), and investment accounts to transactions made through credit cards and bank accounts directly. On top of that, real-time alerts flag inquiries into your credit file across all three major bureaus, with regular credit score updates and reports included as well. Aura also streamlines freezing a child’s credit file, a genuinely useful feature for parents looking to protect a kid’s financial future before they’re old enough to manage it themselves.

Even some of Aura’s identity monitoring features double as credit protection. Identity verification monitoring, for instance, tracks how personal data and a Social Security number are being used, and Aura flags it if someone, whether that’s you or a fraudster, attempts high-risk transactions like payday loans or wire transfers using that identity. All of these protections, and more, are available across Aura’s plans for individuals, couples, and families or groups.

For most people, the breadth of what’s included makes Aura well worth the investment. That said, a couple of limitations are worth knowing before signing up. The credit lock feature only applies to Experian, not Equifax or TransUnion, which leaves a gap in coverage. Aura also sits at a higher price point than some competitors, so if budget is the main concern, that’s worth weighing against everything included in the feature set.

| Identity monitoring | Yes |

|---|---|

| Credit monitoring | Three bureaus |

| Insurance | Up to $1 million per adult |

| Free trial | 14 days |

| Money-back guarantee | 60 days |

Identity Guard is one of our top-rated services for credit monitoring and identity protection. The platform leverages artificial intelligence to proactively detect and flag potential threats before they have a chance to spiral into something more serious.

One of the first things that stood out when we reviewed Identity Guard is how seriously they take the proactive side of identity protection. Rather than just alerting you after something goes wrong, the platform is constantly working in the background to get ahead of threats. On top of your credit reports and scores, it also keeps tabs on your checking, savings, investment, and retirement accounts. That across-the-board visibility flags suspicious activity before it spirals.

Another element we really like about Identity Guard is that they’ll walk you through setting up security freezes with the three major credit bureaus as well as Innovis — a lesser-known monitoring agency. This is extremely helpful since it will prevent fraudsters from accessing your credit files to take out loans or establish new lines of credit in your name. Note — Identity Guard doesn’t actually set up the freeze for you, they’ll just help guide you through the process.

The company offers several tiers of service, so we recommend you take a look at our breakdown of Identity Guard’s pricing and services.

| Identity monitoring | Yes |

|---|---|

| Credit monitoring | 1-bureau or 3-bureau (except Value plan) |

| Insurance | Up to $1 million |

| Free trial | No |

| Money-back guarantee | 60 days (long-term plans) |

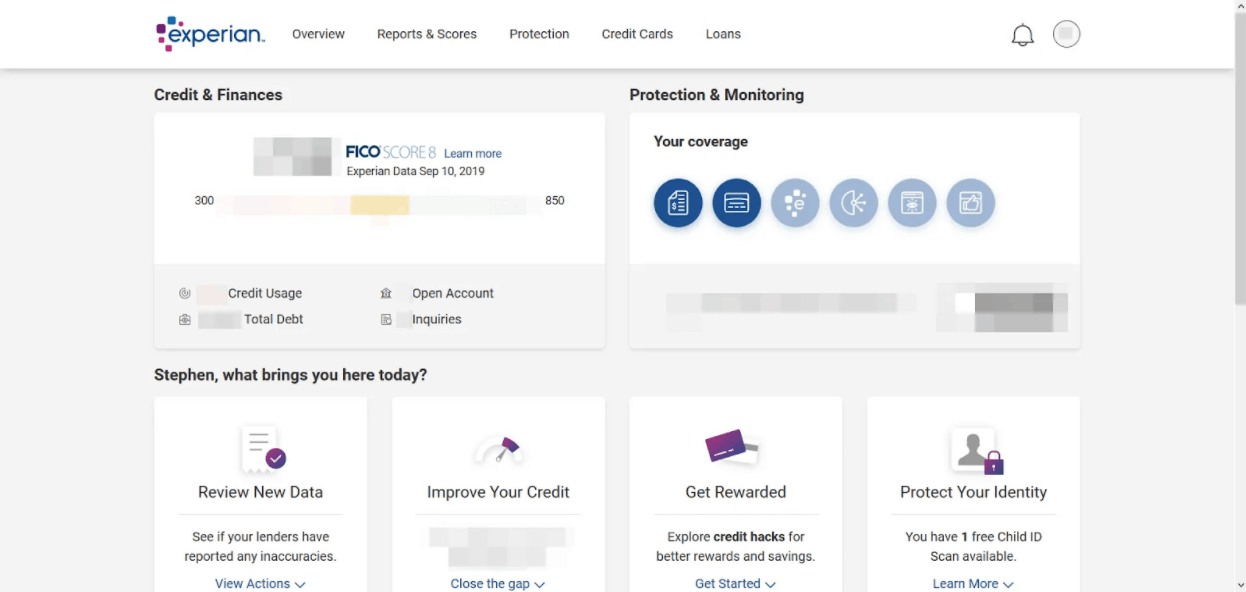

If you want identity theft protection paired with serious credit monitoring, going straight to the source is a smart move. IdentityWorks comes directly from Experian, one of the three major credit bureaus. Plans include real-time alerts, score tracking, and bureau-level monitoring that most third-party services simply can't replicate on their own.

Like we said, since we’re dealing with Experian, you know the credit monitoring is going to be on point. When we tested Experian IdentityWorks, we were pleased to find not only a great core set of services, but some great credit-related add-ons as well. We really appreciated their one-touch Experian credit file lock, their FICO score simulator, and their detailed triple-bureau credit monitoring and reporting.

Another standout feature is Experian Boost. It lets you connect your utility, phone, and even eligible streaming service payments to your Experian credit report. This can give your credit score a meaningful bump — sometimes 15 points or more — essentially overnight.

Did You Know? It’s perfectly normal to see some variation in your credit scores from bureau to bureau. Each agency uses similar data points to calculate your score, but their methodologies vary slightly.

There’s no cookie-cutter approach to identity theft protection, so make sure you check out our guide to Experian IdentityWorks pricing and services to make sure you’re selecting the package that’s right for your specific situation.

| Identity Monitoring | Yes |

|---|---|

| Credit Monitoring | 3-bureau |

| Insurance | $1 million |

| Free Trial | 7 Days |

| Money-back guarantee | None |

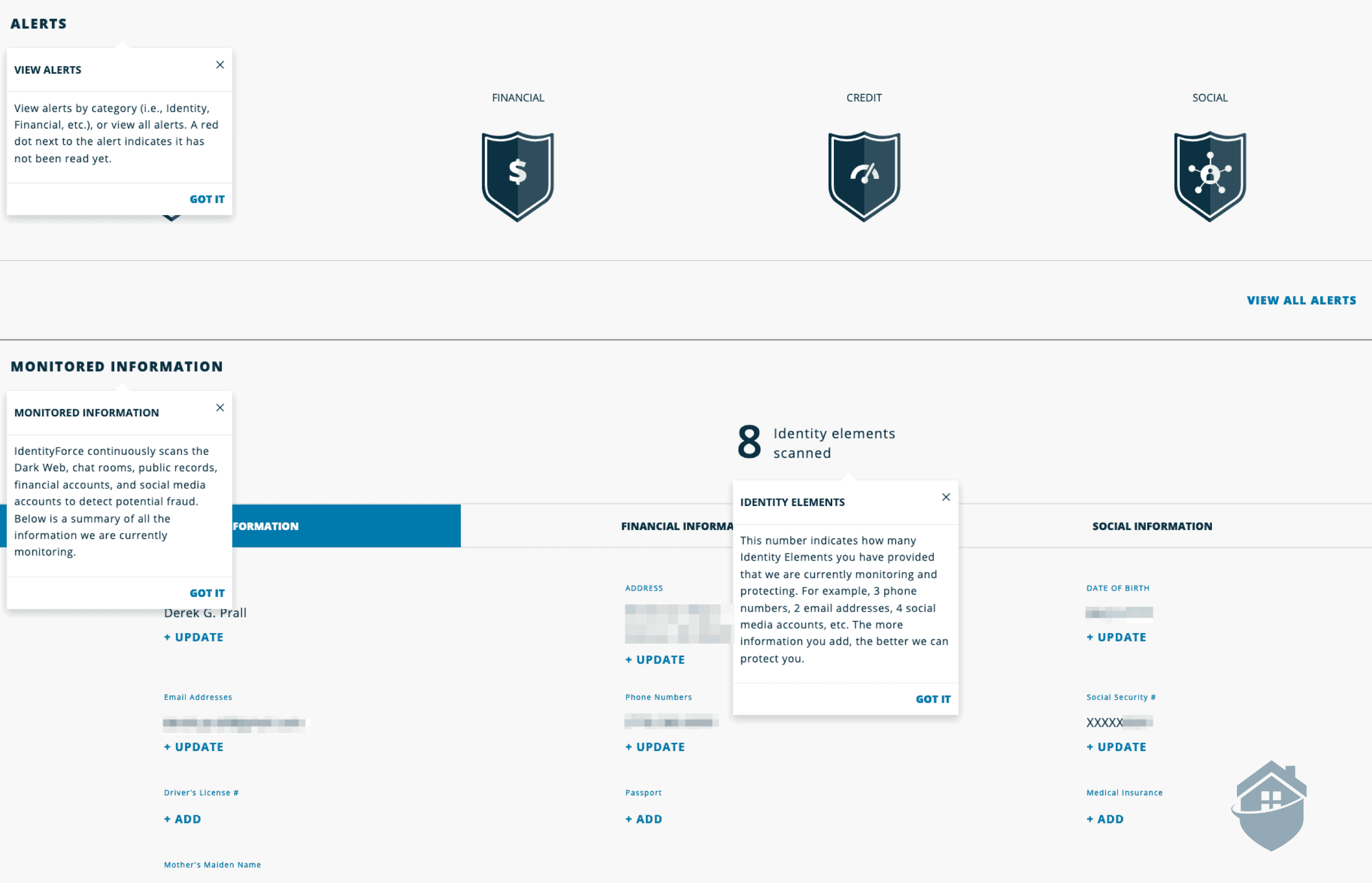

IdentityForce is another powerful identity theft protection service that prioritizes credit monitoring while offering robust protections against all sorts of fraud. Their core functionality is rock-solid, and they offer a few cybersecurity bonuses to boot. Before we unpack their services, let’s take a quick look at the pros and cons punch list.

In our IdentityForce analysis, we found strong protections against a variety of attack vectors that are sure to thwart even the most enterprising identity thief. What we really like, though, is their focus on your finances and on your credit.

You’ll get triple-bureau credit monitoring and reports as expected. However, IdentityForce really stands out with its bonus features. The credit score simulator is one of the most detailed we’ve come across. It gives you a clear picture of how financial moves — like paying down credit card balances or taking out a new loan — could affect your score over time. It’s a genuinely useful tool for anyone actively working to build, repair, or optimize their credit profile.

Did You Know? There are different types of bankruptcy, but they will all negatively impact your credit score for years — some up to a decade. Bankruptcy is really the nuclear option, and should only be used in the most dire of circumstances.

IdentityForce also offers a detailed credit score tracker, so you can take the strategies you’ve developed in the score simulator and see how they impact your numbers over time. Again, a really helpful tool for anyone looking to improve their scores while protecting their identity.

Beyond that, IdentityForce delivers a solid library of financial resources and educational content. While their tools are busy guarding your identity, you can brush up on everything from how mortgages work to tips for scoring a better auto loan rate. This added value separates IdentityForce from a lot of the competition.

Like most protection products on our list, they offer different service packages at different price points. Be sure to check out our breakdown of IdentityForce plans and pricing to make sure you get the best bang for your buck.

| Identity monitoring | Yes |

|---|---|

| Credit monitoring | 3-Bureau |

| Insurance | Up to $2 million |

| Free Trial | 30-Day |

| Money-back guarantee | Yes (prorated) |

PrivacyGuard isn’t as well-known as some of the others on our list, but don’t count them out. We found they offered extremely robust credit monitoring and reporting as well as a full suite of identity theft protections that give some of the bigger names a run for their money. Let’s have a quick look at PrivacyGuard’s pros and cons.

What they’re lacking in name recognition, PrivacyGuard more than makes up for in functionality. While some of the more well known services only offer triple-bureau credit reports once a year, PrivacyGuard grants you access once a month. That’s unique in this space and well worth your consideration if you’re the type that really wants to stay on top of things.

PrivacyGuard also offers a highly detailed triple-bureau credit score tracker so you can see how each of your scores is trending over time. On top of that, you get access to a credit score simulator and a financial calculator suite that can show you how specific financial decisions might affect your score in the future.

Our main gripe is that the entry-level subscription tier doesn’t include any credit bureau monitoring. For comparison, Aura includes three-bureau credit monitoring with all plans. That said, PrivacyGuard’s base plan still gives you useful tools like bank account monitoring, and debit and credit card tracking, so it’s not without value.

A credit report is a document that contains information about your credit activity and current financial situation, including payment histories and the status of your credit accounts. For the most part, these reports are provided by three bureaus — Experian, TransUnion, and Equifax.

Lenders and creditors use your credit report to make a wide range of decisions. It helps inform everything from determining insurance risks and apartment rental approval to loan approvals. In some cases, potential employers may also review your credit report as part of a background check when deciding whether to hire you.

Did You Know? It pays to review your credit report. In fact, after reviewing their credit reports, roughly one in five consumers found an error that could impact their credit scores.2

So, you want to make sure that all of the information on your report is accurate and up-to-date. If it’s not, there might have been a mistake made somewhere along the line, or worse — you might be the victim of identity theft.

When you request your report, it might seem a little complicated at first. That’s okay though, once you know what you’re looking at, things become a little less daunting. Credit reports are divided into four sections, so let’s break those down.

The first section of your credit report is your personal information. This will include your name, any nicknames you go by, your current and former addresses, and sometimes it’ll include your marital status or employment information.

The next section, your credit information — or as they're sometimes called, tradelines — will make up the bulk of the report. This is the information that tells lenders and creditors your history of handling credit accounts. This’ll include a list of your current creditors along with balance information for those accounts as well as payment patterns for the last 24 for 36 months. If you have a late payment or something that has gone to collections, it’ll be indicated in this section.

Next, you’ll find the public records section. This is where anything related to your creditworthiness that shows in your public records will appear. This might include liens, bankruptcies, repossessions, court-ordered child support, or other judgments. Pay close attention to this section. If something doesn’t look right, you’ll want to get it resolved right away.

FYI: Bankruptcy will stay with you for several years, negatively impacting your credit. But bankruptcy is not the end of the world.

Finally, you’ll find your inquiries section. This is a list of anyone who has accessed your credit report. A hard inquiry is one that you authorize — like when you apply for a car loan or mortgage. Soft inquiries, on the other hand, happen when your report is pulled for reasons unrelated to a credit application, such as a background check or a pre-approval offer.

Hard inquiries can temporarily lower your credit score by a few points, so we don’t recommend applying for new credit too frequently. Be sure to pay attention here. If there are hard inquiries you don't recognize, it's a very good indicator that you're the victim of identity theft.

So if you’re being vigilant, you’re checking your credit reports from all three bureaus at least once a year. This will ensure there are no mistakes or fraudulent items negatively impacting your scores.

But what do you do if you find something you don’t recognize? What if there’s something suspicious? Do you have any recourse to dispute your credit report?

The good news is that the three major credit bureaus have dispute processes in place. Disputing an item is completely free, and both the credit bureau and the information provider (the company or organization supplying your financial data to the bureau) are legally required to investigate and respond in a timely manner.

Did You Know? If negative information on your credit report is accurate, it could be there for a while. Most negative information will stick around for up to 7 years, and bankruptcy will appear on your credit report for up to 10 years.

While every situation is unique, generally speaking, disputing an item on your credit report is a two-step process: contacting the bureau, and contacting the information provider.

You'll need to contact the credit bureau in writing with the details you believe are inaccurate. The Federal Trade Commission has a sample dispute letter you can use.3 You can also submit a dispute directly through each bureau's online portal:

You'll need to include copies of any supporting documents that back up your case. From there, the bureau investigates the item by reaching out to the information provider — a process that typically takes around 30 days. While that's happening, notify the information provider in writing that you're disputing the record. They'll also coordinate with the bureau, so everyone stays in the loop.

Did You Know? The best identity theft services offer credit report monitoring and credit score checks so you can stay on top of your creditworthiness. Many will even help you correct errors on your credit report.

While all this is going on, you’ll also need to inform the information provider in writing that you’re disputing a piece of information. You can use the FTC’s sample dispute letter if you’d like. Similar to dealing with the credit bureau, you’ll need to include copies of the documents that support your position. They’ll get in contact with the bureau and everyone will be on the same page.

If you suspect you’re the victim of fraud, there will be other considerations — you might need to contact the federal trade commission or the authorities — but more on that later.

Your credit report is a document containing various data sets that lenders look at to determine your creditworthiness. It absolutely pays to check this report at least once a year to make sure there aren’t any errors and nothing looks out of place.

You're entitled to a free credit report from each of the three major credit bureaus — Experian, TransUnion, and Equifax — every week. You can request your report directly from each agency, or, as the FTC recommends, visit AnnualCreditReport.com to request copies.

If you've never looked at a credit report before, it can feel a little overwhelming. The first section covers your personally identifying information. From there, you'll find the credit account section, where lenders can review your open accounts, mortgages, and loans. After that comes inquiry information, followed by any delinquent accounts or bankruptcies.

In order to establish a new line of credit or take out a loan, a lender does a “hard inquiry” into your credit file. This helps them determine your creditworthiness — or how likely you are to pay back debt — and will inform their decisions whether or not to issue the loan or line of credit and what your interest rate will be.

Did You Know? Hard Inquiries typically lower your credit score by a few points, but that ding will drop off after two years. It’s not a huge deal if you’re applying for a mortgage or taking out an auto loan, but you might want to think twice about applying for a fist full of credit cards all at once.

Now let’s say someone has stolen enough of your personally identifying information to pose as you and applies for a credit card in your name. The credit card company hard-pulls your report, everything looks good, so they issue the fraudster a credit card. They go on a spending spree, never pay the bill, and when it gets sent to collections, the debt collectors start coming after you.

Nightmare, right? Luckily there are a few ways to prevent this from happening, namely credit freezes and credit locks.

Generally speaking, credit freezes and credit locks accomplish the same thing. They prevent creditors and lending agencies from accessing your credit files, and, by extension, prevent unauthorized parties from taking out loans or establishing lines of credit in your name.

Federal law gives you the right to activate and remove credit freezes from each bureau for free. You’ll have to contact each credit bureau individually — Experian, TransUnion, and Equifax — to request them to freeze your credit file. In most cases, this can be done electronically.

Each credit bureau is required to place the freeze within one business day of your request when submitted online or by phone. They'll provide you with a PIN or password you'll need to unfreeze your file. Once requested, they must unfreeze your file within one hour. Just a heads up — if you lose that PIN, you can be issued a new one, but the process to unfreeze your file will take considerably longer.

Locks differ from freezes, but only slightly. They accomplish the same thing, but locks are set and lifted in real-time. Locks are usually set up through third-party vendors like identity theft prevention products or through a secure website or app provided by the credit monitoring bureau. To set up a lock through the credit monitoring bureaus, you’re going to need proof of identification that can be submitted electronically or via hard copies.

Your credit score is a three-digit number that reflects your creditworthiness based on your credit history, payment patterns, and current debt levels. In simple terms, it tells lenders how likely you are to repay borrowed money.

Higher scores signal responsible financial behavior, often resulting in better loan terms, higher credit limits, and lower interest rates. That said, each lender evaluates applicants differently, and your credit score is just one factor in their decision-making process. Generally, scores fall into categories from “Poor” to “Excellent,” helping both you and lenders understand your financial standing at a glance.

In the U.S., three main credit bureaus calculate credit scores using slightly different models. The most widely used scoring system is the FICO score, though VantageScore is also commonly referenced. To access your score, you can check with your bank, request it directly from the bureaus, or use a reputable identity theft protection service like LifeLock, Aura, Identity Guard, or IdentityForce.

Did You Know? It’s perfectly normal for your scores to fluctuate slightly between the three bureaus. While they all use similar data sets, they sometimes weigh specific indicators differently.

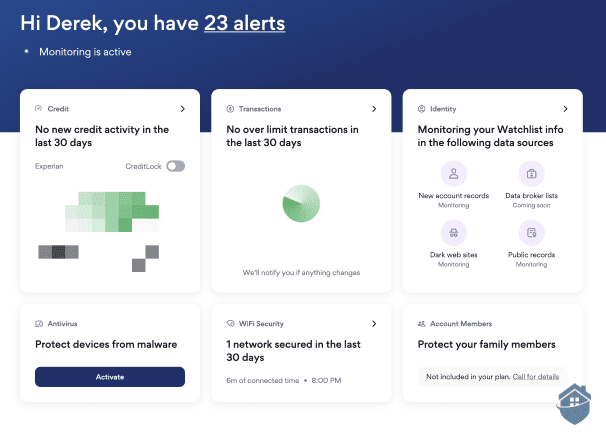

In our experience, the best approach to monitor your credit score is to use a reputable identity theft protection service. Services like LifeLock, Aura, Identity Guard, or IdentityForce provide real-time access to your credit scores and alert you to significant changes.

Monitoring your credit isn't just about loans or interest rates — a sudden drop in your score is often one of the earliest warning signs of identity theft. Catching these signs early gives you the best chance to limit the damage and get ahead of the problem before it spirals.

FYI: Want to find coverage that includes restoration if you happen to fall victim to fraud? You’ll find that these plans all come with up to $1 million in identity theft insurance, dedicated restoration resources, and other benefits should you be targeted by fraudsters.

The following are the most common features of identity theft protection services that include credit protection:

Account fraud and credit theft tend to go hand-in-hand. Bank account takeover is a serious threat — criminals get into your account with the goal of draining it completely. That's why many identity theft services with credit monitoring include features designed to keep unauthorized users out of your accounts before real damage is done. These features typically monitor for suspicious login attempts, unauthorized changes to account credentials, and unusual transaction patterns.

Identity theft services with credit monitoring sometimes offer Payday Loan Monitoring. This feature searches for your name across high-interest loan companies. In the event your name is detected, it’s flagged and you will receive an automatic alert. Taking out loans in someone else’s name is a typical tactic for criminals.

Most services that offer credit monitoring also include credit report monitoring. With this feature, your credit reports from all three major bureaus — Equifax, Experian, and TransUnion — are regularly reviewed. If there's even a hint of suspicious or unusual activity, any new inquiries, or changes to your credit profile, you'll be immediately notified so you can take action fast.

Signing on with just any service with credit monitoring doesn’t mean you’re 100% safe. Fraud still happens. So the smart move is to get covered with identity theft insurance. Some companies put their money where their mouth is with an impressive $1 million policy. This feature could help to bail you out of attorney fees, stolen funds, you name it.

You saved your whole life. You do not want your savings wiped out in one ruthless act of fraud. To avoid this, find an ID theft protection service that offers credit monitoring and 401(k) and investment activity alerts. This suite of features monitors your accounts for suspicious activity and sends automatic alerts if foul play is detected.

A critical feature to say the least, these alerts are triggered when a bank withdrawal, transfer, charge — or really any activity — deviates from your pre-configured settings or dollar amounts.

Identity theft protection companies are stacking their services with Loan Application Monitoring — a brilliant feature that alerts you when a loan application is submitted in your name. Yes, this happens all the time, and it gives a whole new meaning to the term ‘loan shark.’

Your social security number is the key to your identity. So you must protect this key with a robust monitoring service that scans millions (sometimes billions!) of data points looking for your SSN. If it’s found being used by anyone but you, you’ll be alerted immediately.

Federal Trade Commission. (2025). New FTC Data Show a Big Jump in Reported Losses to Fraud to $12.5 Billion in 2024.

https://www.ftc.gov/news-events/news/press-releases/2025/03/new-ftc-data-show-big-jump-reported-losses-fraud-125-billion-2024

National Consumer Law Center. (2026). What States Can Do to Stop Credit Reporting Abuses.

https://www.nclc.org/resources/what-states-can-do-to-stop-credit-reporting-abuses/

Federal Trade Commission. (2024). Sample Letter to Credit Bureaus Disputing Errors on Credit Reports.

https://consumer.ftc.gov/articles/sample-letter-credit-bureaus-disputing-errors-credit-reports